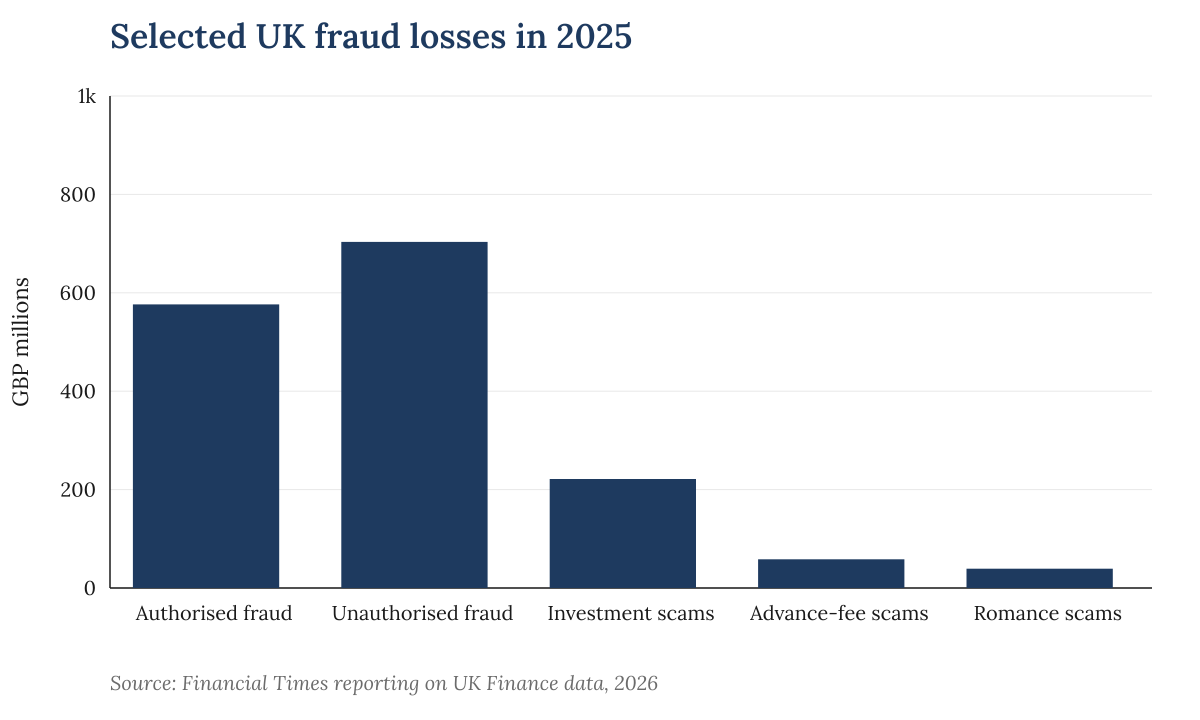

The FT reported that the number of financial-fraud cases rose 11% to almost 4.1mn. It said authorised fraud, where a consumer is tricked into sending money to a criminal-controlled account, rose 19% to GBP 576.4mn. Unauthorised fraud, including card theft and account takeover, fell 5% to GBP 703.4mn.

Selected UK fraud losses in 2025. Source: Financial Times reporting on UK Finance data, 2026.

Selected UK fraud losses in 2025. Source: Financial Times reporting on UK Finance data, 2026.

The fastest-growing reported categories were inside authorised fraud. The FT said investment-scam losses rose 40% to GBP 221.5mn, advance-fee scam losses rose 65% to GBP 58.4mn and romance-scam losses rose 23% to GBP 39.2mn. Those categories are not additional to the authorised-fraud total; they are examples of the losses within it.

The policy dispute is over prevention as much as reimbursement. Authorised push-payment fraud, or APP fraud, is a subset of authorised fraud in which the victim is deceived into making a payment. The Payment Systems Regulator says its APP fraud performance data is intended to show how payment firms perform on APP scams and how they treat victims.

The PSR's reimbursement dashboard says GBP 215mn was reimbursed to APP fraud victims over 2025 and that the percentage of reimbursable APP scam value returned to victims in the fourth quarter was 85%. The regulator says the dashboard monitors the impact of its APP scams reimbursement requirement, rather than measuring all fraud losses in the economy.

The FT reported that the PSR and Financial Conduct Authority had called for technology firms to do more to protect users, while saying banks and telecoms providers must also play their part. UK Finance's Ruth Ray, its managing director for economic crime, told the FT that recent reimbursement changes did not prevent fraud from occurring in the first place and that artificial intelligence was helping criminals scale investment scams.