That is a repricing of supply risk, not proof that supply has normalised. The Guardian's markets coverage reported that Brent fell below $83 and European wholesale gas prices dropped by about 6 percent as investors responded to the prospect of a reopened route. Axios also reported that crude prices fell more than 4 percent to their lowest levels in more than three months after the US and Iran agreed to a ceasefire extension that could lead to the strait reopening.

The market move is easy to understand. The Strait of Hormuz is a critical passage for oil and liquefied natural gas. When it is blocked or unsafe, traders price in physical disruption, insurance costs, longer routes and the risk that inventories will be drawn down. When the route looks likely to reopen, that premium comes out quickly.

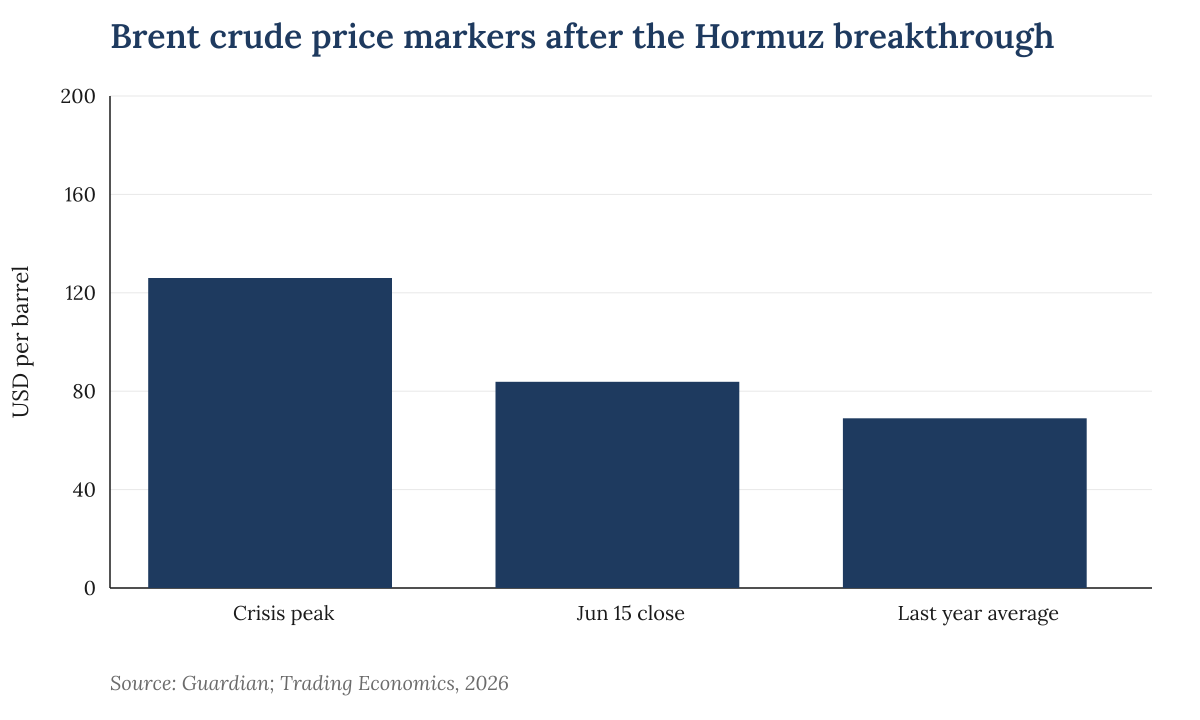

Brent crude price markers after the Hormuz breakthrough. Source: Guardian; Trading Economics, 2026.

Brent crude price markers after the Hormuz breakthrough. Source: Guardian; Trading Economics, 2026.

The slower part is physical. The Guardian separately reported that a return to pre-crisis oil and gas flows could take months even if the strait reopens, because minesweeping, shipping queues and infrastructure damage still have to be resolved. It said Brent had fallen from a crisis peak of $126 a barrel to $82, still above last year's average of $69.

That gap is the economic story. Spot prices can fall on a diplomatic signal; refineries, shipping firms and gas buyers cannot erase months of disruption in a trading session. Tankers have to be cleared, cargoes prioritised and insurance assessed. The Guardian reported that oil tankers and LNG carriers would be prioritised over other goods, and that more than 160 vessels remained stranded. It also reported that damage to Qatar's LNG facilities could slow the recovery in gas exports.