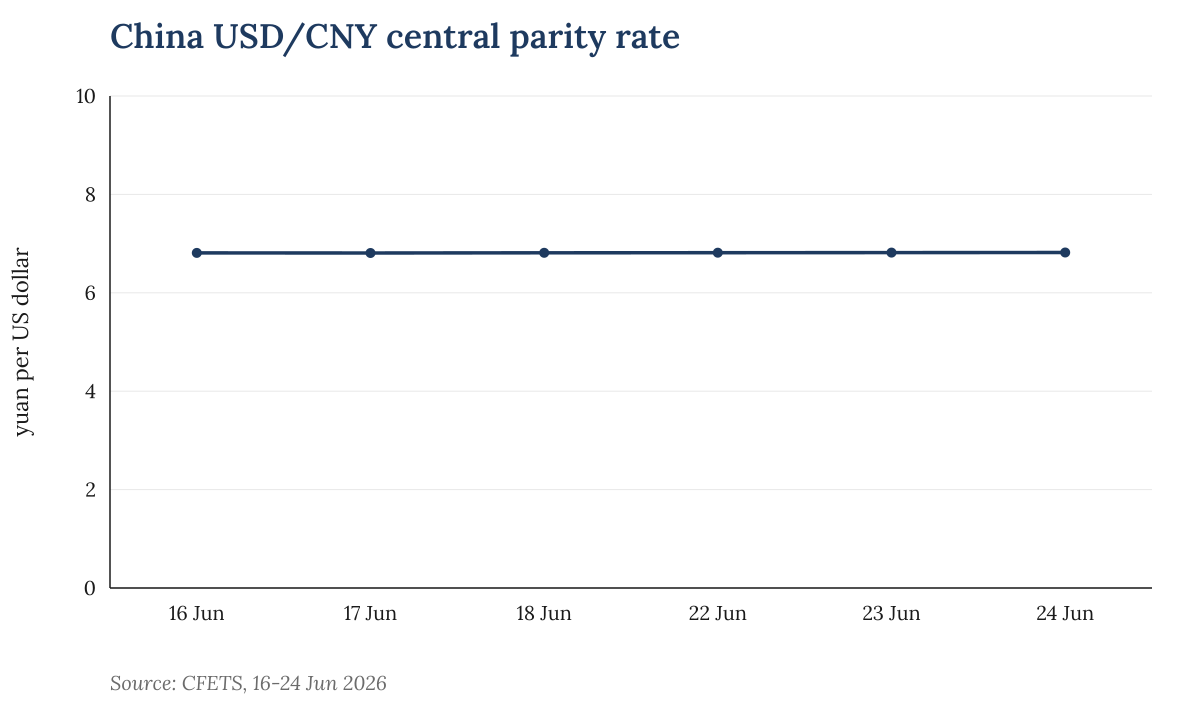

The number is small in market terms; the signal is the point. The central parity rate is the daily reference point around which China's onshore yuan trades, so a sequence of weaker fixings gives investors a window into how much exchange-rate pressure Beijing is willing to absorb rather than resist.

CFETS says it calculates and publishes the central parity rate of the renminbi against the dollar and other major currencies each business day. For the dollar rate, it asks market makers for prices before the domestic foreign-exchange market opens, with those banks referring to the previous day's interbank close, supply and demand, and moves in major currencies. CFETS then excludes the highest and lowest offers and calculates a weighted average of the rest.

The latest week shows a controlled drift rather than a break. CFETS data put the USD/CNY fixing at 6.8108 on 16 June, 6.8096 on 17 June, 6.8130 on 18 June, 6.8150 on 22 June, 6.8171 on 23 June and 6.8195 on 24 June. A higher USD/CNY number means more yuan per dollar, or a weaker yuan fixing against the dollar.

China USD/CNY central parity rate. Source: CFETS, 16-24 Jun 2026.

China USD/CNY central parity rate. Source: CFETS, 16-24 Jun 2026.

The sequence does not, by itself, prove a deliberate devaluation campaign. The Federal Reserve's latest H.10 release showed the dollar's broad index rising from 119.3158 on 15 June to 120.3958 on 18 June, while the Fed's China yuan series moved from 6.7570 to 6.7686 over the same release window. That official US data is not the same as China's daily fixing, but it supports the basic context: the dollar strengthened during the period in which the PBOC's reference rate became less supportive of the yuan.