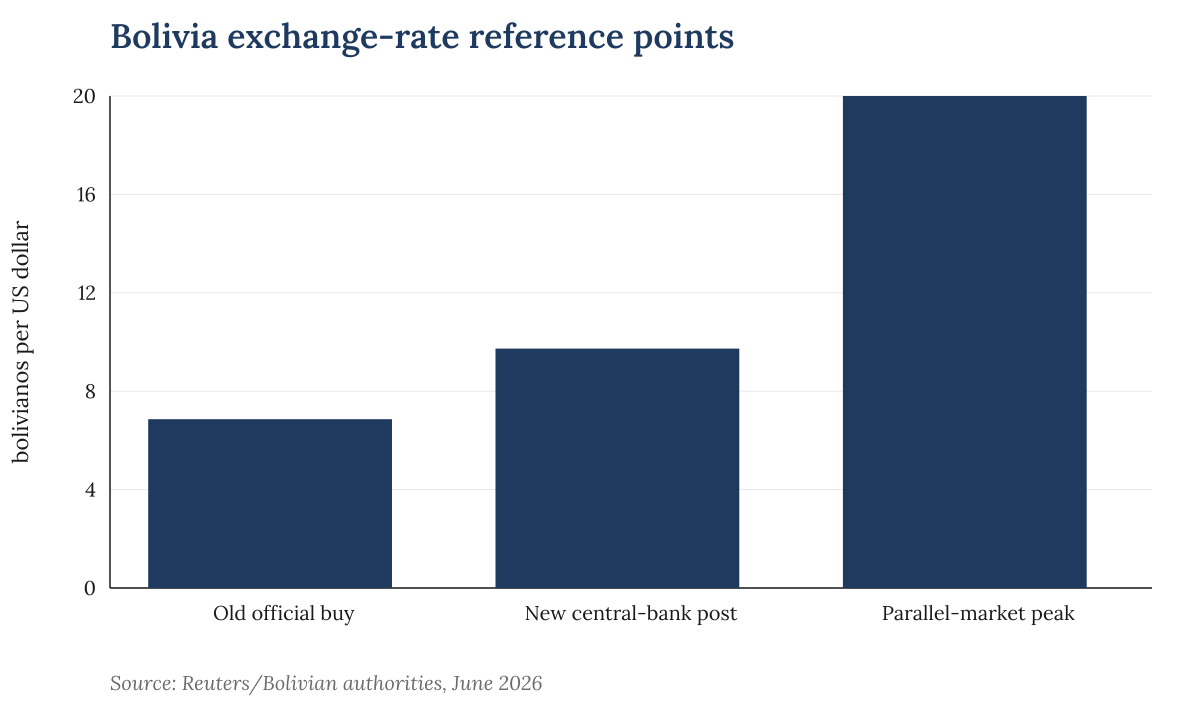

The numbers show why the decision is more than a technical adjustment. Reuters reported that the official rate had been held near 6.86 bolivianos per dollar for buying and 6.96 for selling since 2011. After the change, the central bank posted a rate of roughly 9.73 per dollar, while the parallel market had at times traded near 20. The official move amounts to a large devaluation from the old buy rate, but it still leaves a gap with the price many Bolivians had already seen outside official channels.

Bolivia exchange-rate reference points. Source: Reuters/Bolivian authorities, June 2026.

Bolivia exchange-rate reference points. Source: Reuters/Bolivian authorities, June 2026.

The distinction matters. A flexible system is not automatically a free float, and Bolivia's problem is not solved by changing the label on the currency regime. The test is whether the new mechanism eases pressure on reserves and import payments without feeding a sharper inflation shock through the boliviano.

The old peg had a clear virtue. A stable exchange rate can anchor inflation expectations, especially in a country where households remember periods of high inflation and currency instability. It gives importers, borrowers and wage-setters a simple nominal reference point. The cost is that defending a fixed rate becomes harder when reserves fall or foreign-currency demand rises.

An IMF working paper on Bolivia published in 2022 described the exchange-rate peg as a policy anchor and examined the difficulty of moving between fixed and flexible regimes. That transition problem is now practical rather than academic. If the authorities move too slowly, the official rate can lose credibility against parallel-market prices. If they move too abruptly, imported goods and fuel expectations can push inflation higher.