The Guardian reported on 28 June that about 4,000 local US lenders had joined forces against the CLARITY Act, the House crypto market-structure bill. Their warning is not that Congress failed to regulate stablecoins at all. The GENIUS Act has already created the payment-stablecoin framework and barred issuer-paid yield; the live fight is whether the CLARITY Act and the rulemaking around GENIUS close the rewards channel around exchanges, affiliates and wallets.

That distinction matters because a ban on issuer-paid interest does not settle who can make a stablecoin balance feel yield-like. Community banks argue the gap is outside the issuer. A crypto exchange, broker or affiliated platform could use rewards, rebates or other incentives to make a stablecoin balance feel more attractive than an insured deposit, while claiming the issuer itself has obeyed the statute.

The banking lobby's argument rests on a simple plumbing point. Deposits are not inert balances. They are the cheap, stable funding base that lets local banks lend to small businesses, farms and households. Rebeca Romero Rainey, ICBA's president, told the Guardian that community banks fund more than 60% of small-business loans and 80% of agricultural loans; her question was how those loans get funded if deposits migrate away.

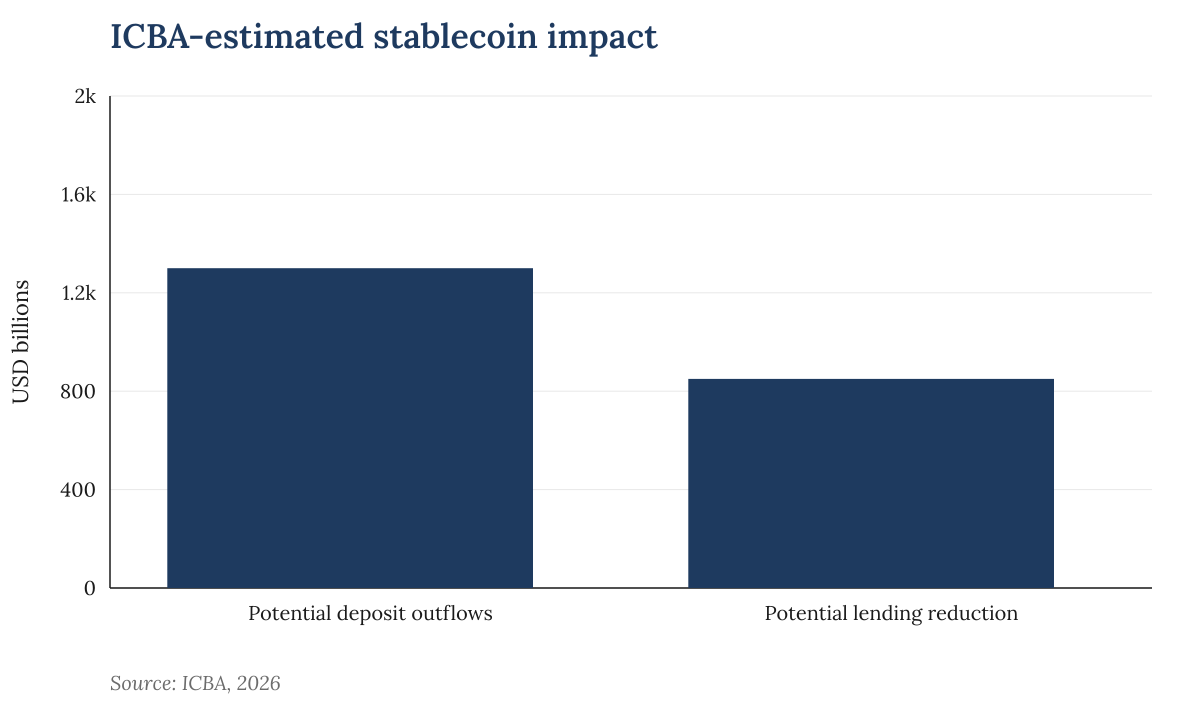

ICBA has put a larger figure on the risk. It estimates that reward-bearing stablecoins could mean $1.3tn in lost deposits and $850bn less lending. Those are advocacy estimates, not observed outflows, but they explain why a drafting question about rewards has become a credit-supply fight.

ICBA-estimated stablecoin impact. Source: ICBA, 2026.

ICBA-estimated stablecoin impact. Source: ICBA, 2026.

The Federal Reserve's weekly H.8 release gives the scale of the funding base at risk, even if it cannot say where stablecoin balances would come from. Small domestically chartered commercial banks held about $5.63tn in deposits in the week to 17 June. They also held about $4.68tn in loans and leases, including roughly $731bn in commercial and industrial loans. Those figures do not prove deposit flight; they show why even a modest migration would be treated as a credit issue rather than a culture-war fight over crypto.