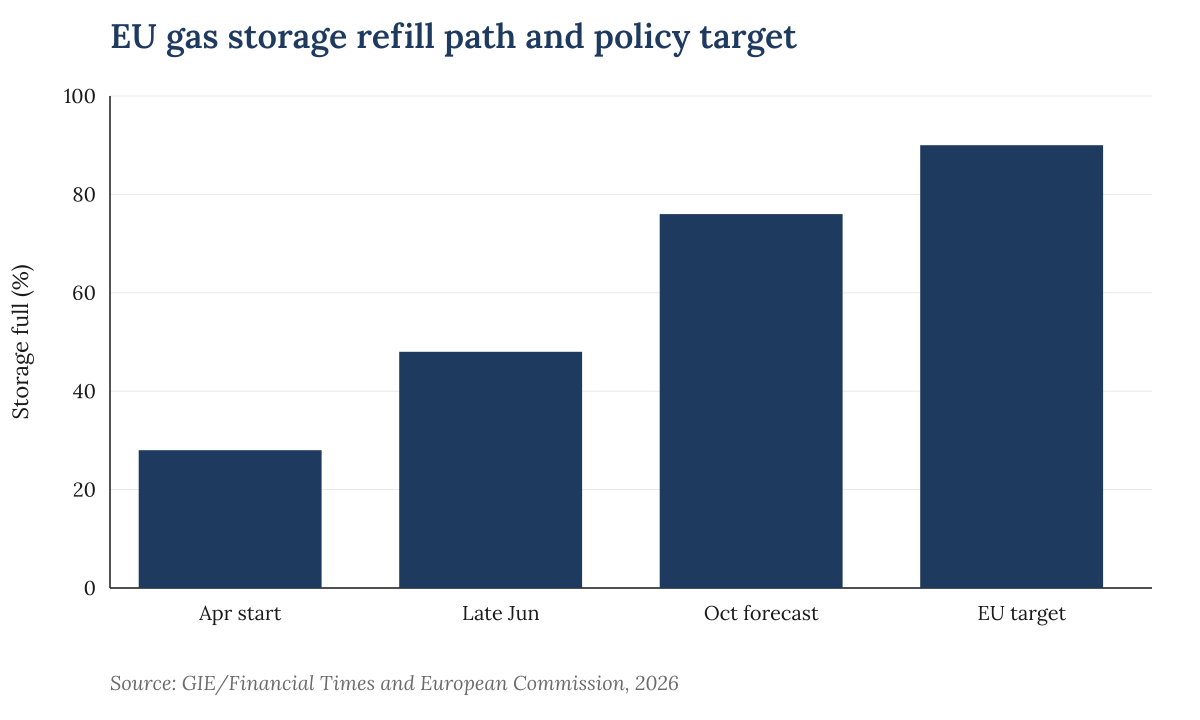

The Financial Times reported on June 29 that Wood Mackenzie expects EU storage sites to end the critical April-to-October restocking season only 76% full. The FT said that would be the lowest peak for stored gas since at least 2011, based on Gas Infrastructure Europe data, and that EU facilities were about 48% full in late June after starting the season at 28%.

EU gas storage refill path and policy target. Source: GIE/Financial Times and European Commission, 2026.

EU gas storage refill path and policy target. Source: GIE/Financial Times and European Commission, 2026.

The European Commission's policy framework explains why that gap matters. It says underground gas storage is central to security of supply, typically providing 25-30% of gas consumed in the EU during winter and reducing the need for additional imports during demand spikes or supply disruptions. The current regulation still sets a 90% annual filling target, though the Commission says the 2025-27 rules give member states a two-month window, from October 1 to December 1, and allow deviations when market or technical conditions make the trajectory difficult.

That flexibility is not cosmetic. Gas Infrastructure Europe said in April that EU storage levels stood at about 28%, or roughly 314TWh and 29bn cubic metres, at the start of the injection season. It said weak or negative summer-winter price spreads were failing to provide enough incentive for early, steady injections, even though storage is the part of the system that provides deliverability when demand rises quickly.

The economics are awkward because the public-policy objective and the private trading signal do not always line up. A utility or trader that buys gas in summer and stores it for winter needs the later price to justify the carrying cost. When the seasonal spread is narrow, the commercial case for rapid injection weakens. Yet the public value of the stored gas is not captured only in that spread: it is insurance against cold weather, supply disruption and competition for liquefied natural gas cargoes.